Espinoza v. Montana Department of Revenue

Argument: January 22, 2020

Petitioner Brief: Kendra Espinoza, et al.

Respondent Brief: Montana Department of Revenue, et al.

Decision: TBA

Court below: Supreme Court of the State of Montana

Montana faces Establishment Clause questions over a tax credit program

Montana established a tax credit program that allows people to donate to a scholarship fund for students attending private schools. In return, the taxpayer receives a matching tax credit of up to $150. The scholarship fund provides scholarships to private school students, including those who attend religious private schools.

Montana’s Department of Revenue was tasked with administering the tax credit program. When it began working to carry out the program, it realized the program — as written by Montana’s legislature — came into conflict with the Montana Constitution.

The Montana Constitution includes a provision called the “Blaine Amendment.” The Blaine Amendment prohibits the state from using any state funds to “directly or indirectly” benefit a sectarian/religious purpose. The tax credit program planned to disburse scholarships to be used at private religious schools, which would indirectly benefit sectarian purposes.

To address the conflict with the Montana Constitution, the Montana Department of Revenue issued a rule, called “Rule 1.” Rule 1 said that the scholarship program could not fund scholarships at religious schools. The tax credit program would fund scholarships at nonreligious private schools only.

The lawsuit

Parents of children who attend religious private schools sued the Montana Department of Revenue. They argued that Rule 1 violates the U.S. Constitution. Rule 1 acts with hostility towards religion, which the Constitution does not allow. Of course, the plaintiffs admit, the Establishment Clause says the government cannot endorse religion or any particular religion, but the government can act neutrally towards religion. That’s what the tax credit program did originally, by not making a distinction of religion at all.

Plaintiffs continue that the First Amendment contains another requirement to ensure the Free Exercise of religion. Ensuring free exercise, thus, means the government cannot single out religious schools and forbid the tax program from benefiting them. Rule 1 does just that, whereas the original tax program acted neutrally towards religion.

The plaintiffs point to the Equal Protection clause too: the government cannot treat religious groups differently than non-religious groups. When the Blaine Amendment goes so far as to prohibit a neutral tax program from benefiting people based on their religion, then it has been used unconstitutionally. The United States Constitution prevails over the Montana Constitution, which means, as the plaintiffs argue, Montana’s Rule 1 is invalid.

Tension between the Free Exercise Clause and the Establishment Clause

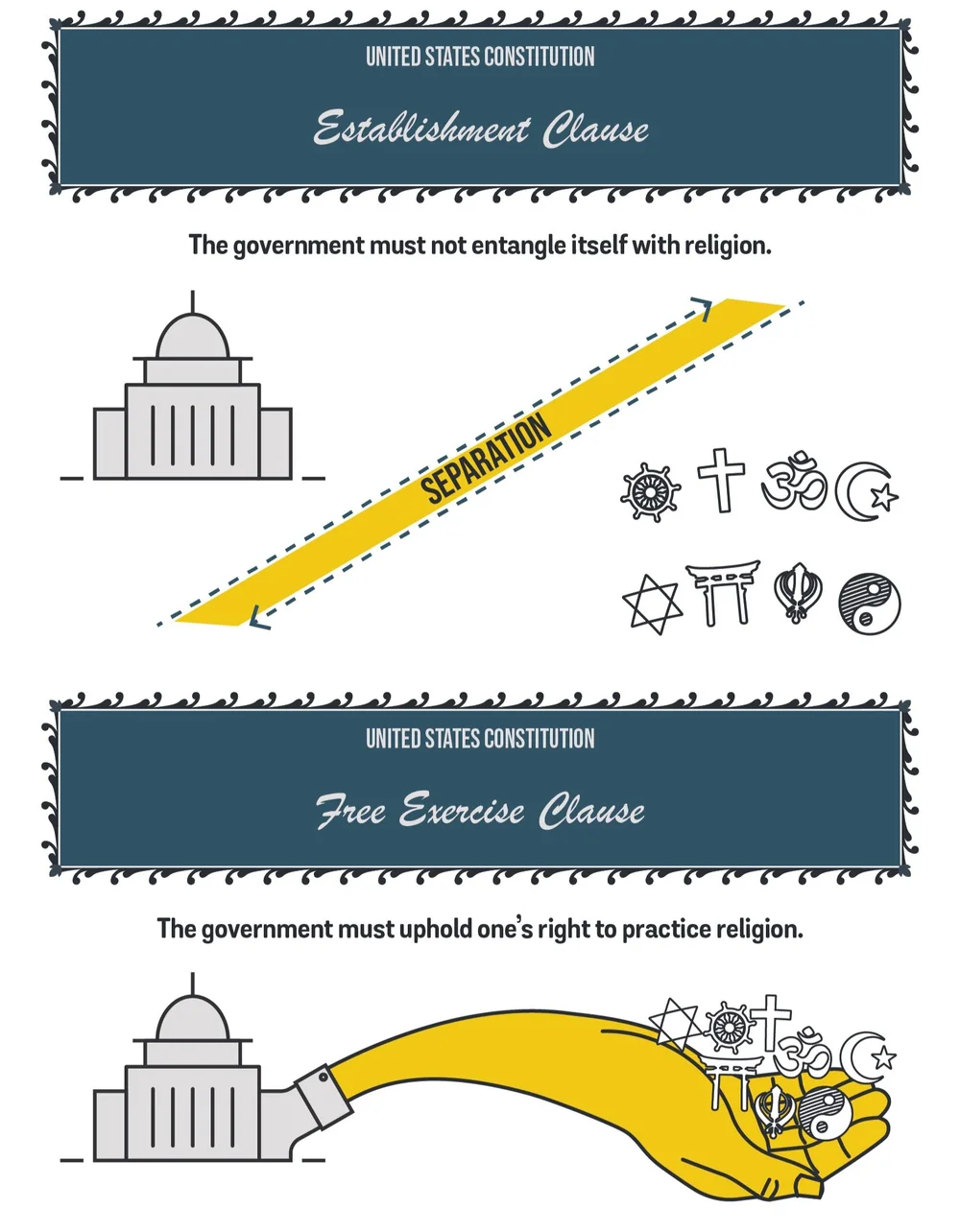

The Establishment Clause requires the government to stay out of religion, and the Free Exercise Clause tells the government to ensure people can practice freely. How can the government both avoid religion and uphold it at the same time?

The answer depends on how strictly one interprets the Establishment Clause. How strong must the “wall of separation” between the government and religion be?

The government cannot sponsor “excessive entanglement” with religion, but does that mean the government can’t ever indirectly benefit any religious purposes?

The Blaine Amendment

The Blaine Amendment imposes a strong interpretation of the wall between the government and religion. No government money can cross the wall.

Is it possible that the wall of separation required by the Blaine Amendment is so strong as to come into conflict with Free Exercise and other parts of the Constitution? The plaintiffs are not asking the Supreme Court to invalidate the Blaine Amendment entirely, but they argued to the trial court that the Montana Department of Revenue’s use of the Blaine Amendment to make the tax program “hostile” towards religion was unconstitutional.

Procedural history

In the trial court, the plaintiffs won. The Montana trial court ruled that the Department of Revenue’s Rule 1 violated the U.S. Constitution by excluding religious schools from the tax credit program.

However the Montana Supreme Court reversed the ruling. The Montana Supreme Court ruled that the tax credit program as originally written violated the Blaine Amendment. Thus, the court invalidated the original tax credit program. It said the Montana Department of Revenue didn’t even have the authority to create Rule 1 because Rule 1 was a significant departure from what the legislature intended. The Montana Supreme Court left the state without a tax program to fund school scholarships at all. Not for religious schools and also not for nonreligious schools.

Question in the Supreme Court

The plaintiffs were not happy with the ruling by the Montana Supreme Court. They appeal now to the Supreme Court, saying the Montana Supreme Court’s ruling is also hostile towards religion. The Montana Supreme Court invalidated an entire tax program — a religiously-neutral one — just because students have the choice to use the scholarships at religious schools. Like Rule 1, that action is hostile towards religion, the plaintiffs claim, and they petition the Supreme Court for help.

Defending the Montana Supreme Court ruling, the Montana Department of Revenue says the plaintiffs cannot complain of being treated unfairly because now no one has a tax program. It’s not discriminatory towards religion because the program is erased. It can’t violate the Equal Protection clause because the non-program treats everyone equally.

This is different than the situation in Trinity Lutheran Church v. Comer, Montana argues, where the Supreme Court invalidated a Missouri rule prohibiting public funds from resurfacing a playground at a church daycare. In Trinity Lutheran, the public funds were going to resurface playgrounds at some schools, just not religiously-affiliated ones. In contrast, in this case, there’s no money going anywhere, so the current state does not offend the Constitution.

The Supreme Court will hear arguments on January 22, 2020.

Establishment Clause Reports:

fromSubscript Law Blog | Subscript Lawhttps://https://ift.tt/2TG5Iul

Subscript Law

4 Curtis Terrace Montclair

NJ 07042

(201) 840-8182

https://ift.tt/2oX7jPi

Comments

Post a Comment